Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 23 on the introduction.

On page 24 Piketty might be pulling a bit of linguistic sleight of hand mixing labor with remuneration. As Piketty defines it on page 18, labor is "wages, salaries, bonuses, earnings from nonwage labor, and other remuneration statutorily classified as labor related." A large chunk of these high remuneration packages are set as stock options which, at least under highly influential New York law are not wages. Is Piketty going to be correcting for that in the US and UK data where such forms of compensation are more prevalent? Again, early in the book, but it will be really easy not to make that adjustment but for a book that is so generously footnoted, it's disappointing that a note doesn't cover the issue here. Curing the disconnect between remuneration and firm performance would seem to encourage a shift to non-labor remuneration in the form of stock options. This is unlikely to be an attractive solution for Piketty but why wouldn't that help cure one of his divergent forces on inequality?

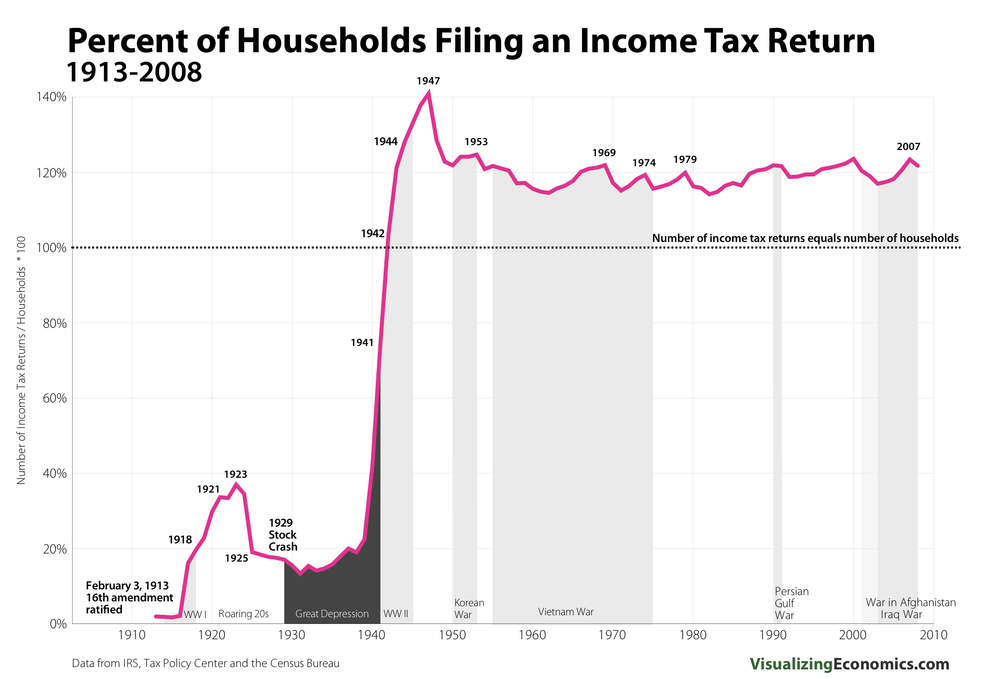

Piketty's first chart appears on this page, a chart showing income inequality in the United States from 1910-2010. I think it is relevant to match Piketty's data with the number of people who actually had to file.

Clearly the early data is very sparse, in 1913 as low as 2% of households filed. Is it coincidental that the WW II era explosion of number of returns coincides with Piketty's chart that features a remarkably sharp decline in inequality? Or has Piketty pushed his chart beyond the reasonable limits of available data?

I don't have any particular insight into the sparseness of data for Piketty's second chart but the first chart tells me that somebody should check the numbers and ask the relevant question, whether the early portion of the data is as questionable as his first chart looks to my eyes. Piketty himself notes that his data is not as widespread as he would like it to be. It would have been responsible to add a line between the years of robust data availability and the zones where caution is warranted. It is a responsibility that Piketty seems uninterested in meeting. Perhaps such things will be added in a 2nd edition.

On page 27, Piketty errs when he says "the fundamental R > G inequality, the main force of divergence in my theory, has nothing to do with any market imperfection." There is a market imperfection. It is real. By saying that there is no market imperfection, Piketty is implicitly excluding the laboring class from joining the investor class and making an artificial barrier into a natural barrier. The laborer shall be the laborer and never a capitalist. The world does not work this way.

Piketty has to explain Andrew Carnegie, who started as a telegrapher and became one of his age's foremost capitalists as well as all the other famous and not so famous self-made men who have made the transition. From all I have read, he never addresses this change of role potential.

Piketty claims that the rapid growth of population in the US from 3M at the time of the Declaration of Independence, and the rapid growth of territory from the 13 colonies to the addition of Alaska and Hawaii in the 1950s make the US experience a non-generalizable outlier and that the correct model to look at the general world case is slow to expand France which only doubled its population during the same time period. The territory changes of France with the addition and subtraction of its colonial possessions is tastefully left out of the discussion. It likely would only confuse the narrative.

Of course by a priori excluding the US example as a model going forward, Piketty is cheating. He does not bother to prove his justification for excluding the US. It's just declare it as a non-generalizable outlier and move on.

I do agree with Piketty on the importance of gathering data and using the real world to inform and judge theories. A pretty theory that doesn't work and thus should be jettisoned is a global attitude that would have saved us from the gulag and would resolve the present problems of both North Korea and Cuba. But Piketty is only imperfectly applying his own standards here. He should be held strictly to them. For instance, he declares that the changes in US territory and demography lead it to be "no longer the same country". So how many countries is it and what is the data for each of those virtual countries? There is no data presented.

Does R > G indicate a shortage of capital or a surplus of capital? It would seem obvious to me that this status indicates a shortage, but the cure that Piketty prescribes would indicate that he believes that it indicates a surplus. You raise taxes on what you want less of. Perhaps I simply misunderstand and R > G can happen whether capital is in surplus or shortage, ie there is no relationship. I do not see how that can be true but I'm willing to be persuaded if Piketty ever gets around to addressing a small matter such as this.

This concludes my examination of Piketty's Introduction to Capital in the Twenty-First Century. I picked up the project because I had a surplus of time on my hands as I was waiting for some very long database reindexes. If this occurs again, I may pick up the book and proceed further but for now this will be the end of this series.

No comments:

Post a Comment