I've been remarking for a couple of years that the flow of jobs will reverse and poor areas in the US will start to see work moving from China. What I had in mind was returning US companies. But there seems to be an unexpected bonus. The Chinese are coming.

I should have seen it from the first. If it's cheaper for a US company to build something in the US, it's going to be just as advantageous for China's private businesses to do the same. So why not expand abroad and reduce their political risk while improving their profitability?

Wednesday, June 25, 2014

Tuesday, June 24, 2014

Fixing the data loss loophole

The US Congress could, with a pretty small outlay of money, set up a web portal with an API that would allow all executive branches to report data losses within a few days of when they happened. And then we should require that they report within 5 days. We could call it Lois' law.

Most recently this would have had the effect of chopping two years off the timeline of the IRS scandal and perhaps made it a live issue for the 2012 campaign. Big data analytics might also be deployed on this database to find "data loss hot spots" and better direct where to deploy investigative efforts. The bonus, a lot of hard drives are over $100 dollars so just destroying one is a crime sporting a ten year prison term. You have a lot of leverage at that point to play 'make a deal' in order to get at the underlying politically motivated crimes.

Saturday, June 21, 2014

Bitcoin as US currency warfare

Still noodling around with bitcoin and learning more about the phenomenon. One of the puzzlers that a number of people are scratching their head about is the cautious support that bitcoin seems to be getting in the US. Why would an inherently deflationary currency attract support from a government that seems so strongly committed to inflating its currency into a creeping devaluation.

The answer came in an hour long talk with Andreas Antonopoulos that was up on youtube. He forthrightly predicted that bitcoin was eroding all currencies but that the dollar would be the last to fall. In the 'devil take the hindmost' currency world we inhabit, that makes bitcoin an ally of the Fed for now.

Things do seem to be playing out that way as China subsequently made moves against bitcoin even as it also made moves to work with Russia to supplant the dollar.

How big is bitcoin? Saturday June 21, 2014

For this post all values are rounded.

As of today bitcoin has created

12,922,000 coins in circulation

At time of writing 1 bitcoin was $594 USD

This puts the total value of the coins at $7.7 billion USD and is roughly equivalent to what the federal reserve calls M0. For USD M0 is $3.9 trillion at present.

If Bitcoin were an economy, it would be the 149th largest in the world slightly larger than Montenegro and slightly smaller than Mauritania.

As of today bitcoin has created

12,922,000 coins in circulation

At time of writing 1 bitcoin was $594 USD

This puts the total value of the coins at $7.7 billion USD and is roughly equivalent to what the federal reserve calls M0. For USD M0 is $3.9 trillion at present.

If Bitcoin were an economy, it would be the 149th largest in the world slightly larger than Montenegro and slightly smaller than Mauritania.

Ethereum - Bitcoin on steroids

Bitcoin was only the beginning

Ethereum is bitcoin style disruption (blockchain technology) that is generic across anything writable in software. That's huge.

Etherum is not ripe. It's not something you want to devote a lot of resources to but it is something you want to keep your eyes on to monitor because any successful etherum software can disrupt any field of endeavor as bitcoin is disrupting banking. Look to hear about ethereum in a mainstream news outlet near you in mid 2015.

Tuesday, June 17, 2014

What is Bitcoin?

Bitcoin is not what you think it is. This is the sort of thing that comes out when you listen to Bitcoin insiders who actually build the software that makes Bitcoin a thing.

Everyone in this room understands that Bitcoin is not a currency. It is a value transfer network with a decentralized consensus mechanism.Translating from techno-geek to poli-geek, Bitcoin makes voluntary polities. In plain english it allows people to congregate into one or more novel, voluntary associations, entering and exiting them at will.

The point of doing that is to establish convenient states of "we" as in we dollar spenders, we mastercard holders, and even we believers in this or that social habit or norm. This is incredibly valuable. It allows participants to exchange value within an enhanced trust set of rules. In the real world, this is a more granular edition of what european countries faced when they looked at joining the euro zone. A number of countries for whom joining was economically a bad idea did it anyway because they saw advantage in adopting a shared identity. Greek euro bonds suddenly sold at nearly the same low interest rates as German euro bonds. The market priced nation state bonds by the identity, and the repayment risk, of the most trustworthy of the big euro economies for years. It took the admission of a massive violation of trust and the rules of the euro (Greece's accounting fraud scandal) before national bond pricing was restored.

In this view, nation-states create a massive bundle of shared values, and a number of them are expressed through the currency. Bitcoin as software allows anyone to express shared values, sometimes economic, sometimes as expressions of solidarity. The politics of which shared values will be expressed is independent of the software. It pretty much can be anything.

Wednesday, June 11, 2014

Tea Party Comprehensive Immigration Reform

I'm an immigrant, but not much of one. We left Romania, legally, in 1971 through the grace of God and Richard Nixon. Essentially I was part of the communist slave trade because we were in bondage and, arriving in the US, we became free.

My aunt argued against it. Why she argued against it and why she was wrong provides the core of a Tea Party immigration policy that is in the United States' interest, comprehensive, and humane.

There are people who fall in love from afar. My father is like that with the USA. My family's tale of immigration starts with my grandmother running from an intolerable personal situation and my grandfather following her. My two aunts were born in the US. My family returned to Romania in a case of pretty bad timing, just in time for the bottom to drop out as the Great Depression started soon after. My father grew up on stories of America and what it was like there and when my aunts became adults, they eventually got their US passports and left.

The soft costs of immigration to the immigrant and family ripple across a generation or two. There is a loss of social context, a feeling of not entirely belonging. You're the outsider, the stranger. Both cultures are home but neither culture entirely fits. Unless you are like my grandmother and desperate or like my father and in love, these soft costs dominate the equation and people just don't move very often.

Essentially my father was an american long before he set foot on US soil. He loves this country, became naturalized, learned english, had a long career as a civil engineer, and did his best to make America a better place. He's the sort of immigrant that contributed far more than he took and is a significant chunk of the conservative movement. He's also a minority of immigrants crossing the border today. Such love affairs have always been a minority but they are an important minority to recognize and embrace because they falsify the narrative of the Tea Party's enemies that it is cruel and unfeeling and only interested in simplistic solutions that have no soul.

The desperate, on the other hand, are dangerous. Desperate people can swamp a boat, collapse a bridge, trample people to death. Talk to anybody who does work in crowd control and they'll tell you desperate people in large numbers can be scary dangerous. The crowd control professionals have all sorts of multi-layer strategies to prevent, reduce, channel, and contain the consequences of crowds gone wrong (desperation is shorthand for a number of emotions, the common point being that they shut down rational thought and good sense).

My aunt argued against it. Why she argued against it and why she was wrong provides the core of a Tea Party immigration policy that is in the United States' interest, comprehensive, and humane.

There are people who fall in love from afar. My father is like that with the USA. My family's tale of immigration starts with my grandmother running from an intolerable personal situation and my grandfather following her. My two aunts were born in the US. My family returned to Romania in a case of pretty bad timing, just in time for the bottom to drop out as the Great Depression started soon after. My father grew up on stories of America and what it was like there and when my aunts became adults, they eventually got their US passports and left.

The soft costs of immigration to the immigrant and family ripple across a generation or two. There is a loss of social context, a feeling of not entirely belonging. You're the outsider, the stranger. Both cultures are home but neither culture entirely fits. Unless you are like my grandmother and desperate or like my father and in love, these soft costs dominate the equation and people just don't move very often.

Essentially my father was an american long before he set foot on US soil. He loves this country, became naturalized, learned english, had a long career as a civil engineer, and did his best to make America a better place. He's the sort of immigrant that contributed far more than he took and is a significant chunk of the conservative movement. He's also a minority of immigrants crossing the border today. Such love affairs have always been a minority but they are an important minority to recognize and embrace because they falsify the narrative of the Tea Party's enemies that it is cruel and unfeeling and only interested in simplistic solutions that have no soul.

The desperate, on the other hand, are dangerous. Desperate people can swamp a boat, collapse a bridge, trample people to death. Talk to anybody who does work in crowd control and they'll tell you desperate people in large numbers can be scary dangerous. The crowd control professionals have all sorts of multi-layer strategies to prevent, reduce, channel, and contain the consequences of crowds gone wrong (desperation is shorthand for a number of emotions, the common point being that they shut down rational thought and good sense).

Monday, June 9, 2014

Piketty's Introduction - Part IV

This is a four part series going through Thomas Piketty's Capital in the 21st Century the parts can be found here:

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 23 on the introduction.

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 23 on the introduction.

On page 24 Piketty might be pulling a bit of linguistic sleight of hand mixing labor with remuneration. As Piketty defines it on page 18, labor is "wages, salaries, bonuses, earnings from nonwage labor, and other remuneration statutorily classified as labor related." A large chunk of these high remuneration packages are set as stock options which, at least under highly influential New York law are not wages. Is Piketty going to be correcting for that in the US and UK data where such forms of compensation are more prevalent? Again, early in the book, but it will be really easy not to make that adjustment but for a book that is so generously footnoted, it's disappointing that a note doesn't cover the issue here. Curing the disconnect between remuneration and firm performance would seem to encourage a shift to non-labor remuneration in the form of stock options. This is unlikely to be an attractive solution for Piketty but why wouldn't that help cure one of his divergent forces on inequality?

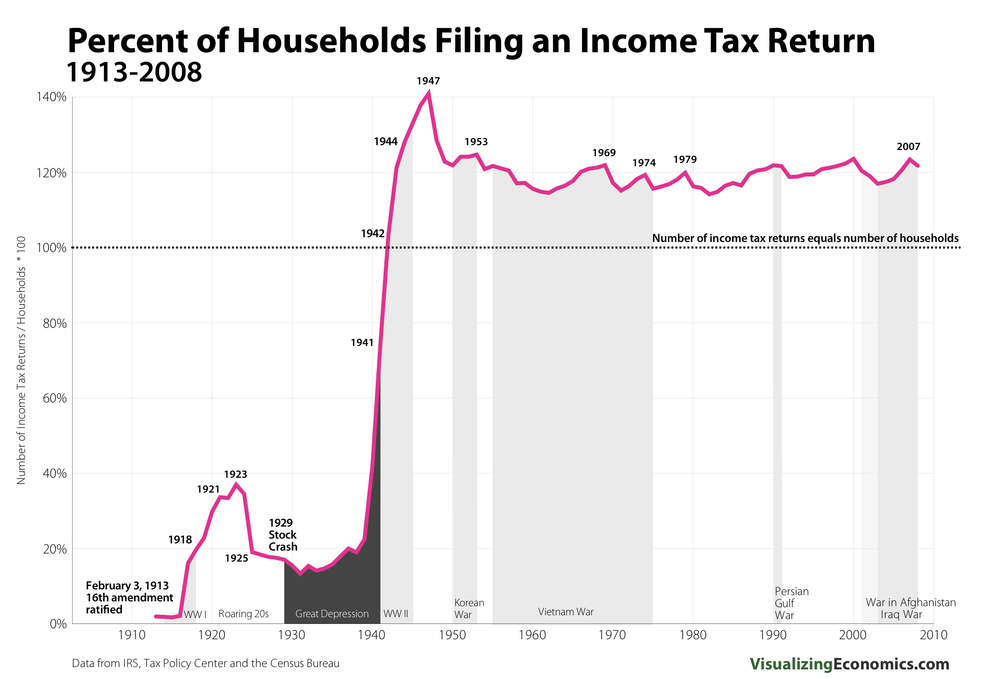

Piketty's first chart appears on this page, a chart showing income inequality in the United States from 1910-2010. I think it is relevant to match Piketty's data with the number of people who actually had to file.

Clearly the early data is very sparse, in 1913 as low as 2% of households filed. Is it coincidental that the WW II era explosion of number of returns coincides with Piketty's chart that features a remarkably sharp decline in inequality? Or has Piketty pushed his chart beyond the reasonable limits of available data?

I don't have any particular insight into the sparseness of data for Piketty's second chart but the first chart tells me that somebody should check the numbers and ask the relevant question, whether the early portion of the data is as questionable as his first chart looks to my eyes. Piketty himself notes that his data is not as widespread as he would like it to be. It would have been responsible to add a line between the years of robust data availability and the zones where caution is warranted. It is a responsibility that Piketty seems uninterested in meeting. Perhaps such things will be added in a 2nd edition.

On page 27, Piketty errs when he says "the fundamental R > G inequality, the main force of divergence in my theory, has nothing to do with any market imperfection." There is a market imperfection. It is real. By saying that there is no market imperfection, Piketty is implicitly excluding the laboring class from joining the investor class and making an artificial barrier into a natural barrier. The laborer shall be the laborer and never a capitalist. The world does not work this way.

Piketty has to explain Andrew Carnegie, who started as a telegrapher and became one of his age's foremost capitalists as well as all the other famous and not so famous self-made men who have made the transition. From all I have read, he never addresses this change of role potential.

Piketty claims that the rapid growth of population in the US from 3M at the time of the Declaration of Independence, and the rapid growth of territory from the 13 colonies to the addition of Alaska and Hawaii in the 1950s make the US experience a non-generalizable outlier and that the correct model to look at the general world case is slow to expand France which only doubled its population during the same time period. The territory changes of France with the addition and subtraction of its colonial possessions is tastefully left out of the discussion. It likely would only confuse the narrative.

Of course by a priori excluding the US example as a model going forward, Piketty is cheating. He does not bother to prove his justification for excluding the US. It's just declare it as a non-generalizable outlier and move on.

I do agree with Piketty on the importance of gathering data and using the real world to inform and judge theories. A pretty theory that doesn't work and thus should be jettisoned is a global attitude that would have saved us from the gulag and would resolve the present problems of both North Korea and Cuba. But Piketty is only imperfectly applying his own standards here. He should be held strictly to them. For instance, he declares that the changes in US territory and demography lead it to be "no longer the same country". So how many countries is it and what is the data for each of those virtual countries? There is no data presented.

Does R > G indicate a shortage of capital or a surplus of capital? It would seem obvious to me that this status indicates a shortage, but the cure that Piketty prescribes would indicate that he believes that it indicates a surplus. You raise taxes on what you want less of. Perhaps I simply misunderstand and R > G can happen whether capital is in surplus or shortage, ie there is no relationship. I do not see how that can be true but I'm willing to be persuaded if Piketty ever gets around to addressing a small matter such as this.

This concludes my examination of Piketty's Introduction to Capital in the Twenty-First Century. I picked up the project because I had a surplus of time on my hands as I was waiting for some very long database reindexes. If this occurs again, I may pick up the book and proceed further but for now this will be the end of this series.

Sunday, June 8, 2014

Piketty's Introduction - Part III

This is a four part series going through Thomas Piketty's Capital in the 21st Century the parts can be found here:

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 15 on the introduction.

On page 15 there's an interesting concept introduced of "inequalities at the global level" that leaves me scratching my head. China "may well prove to be a potent force for reducing inequalities on the global level" but isn't China's turning towards capitalism mean that its headed towards more inequality? What is different (superior?) about the Chinese road towards the market? Before Deng, what was China's role regarding inequality on a global level? I would hope that Piketty explores this more fully later. We'll see.

The idea that you can make any sort of straight line trends in global economics last 35 years, much less 85 years with a straight face is in my mind, well, naive at best. But Piketty goes for it even as he makes sure to inject enough uncertainty in his projections to make this statement meaningful. In other words, he's dog whistling about the world ending up being owned due to the straight line projection across several decades. If anybody of influence were to call him on this, no doubt he would retreat, and quickly. From the media appearances I've observed, he's obviously not enough of an idiot to defend such a declaration, though he is enough of one to have made it in the first place.

An interesting assumption embedded in Piketty's snark about Solow and Kuznets "balanced growth path" is that the rich world is advanced in the sense that Solow and Kuznets meant. That's not actually proven. For instance in the 1970s, the US made a retrograde move that established an oligarchy in bond rating agencies, one that continues to this day. How many other retrograde moves have been made and what does that mean in the sense of the Kuznets curve? There's plenty of pages to go and perhaps Piketty addresses this later but it is as absurd to assume that capitalism is a one way road. As Newsweek famously observed in 2009 "we are all socialists now." Has this socialism turned back the clock on the Kuznets curve? Is that even on Piketty's radar?

The 19th century economists, especially Marx, underestimated the mobility of people to change roles when the legal system permits them to and the economic system incentivises them to. Our economy would be more balanced if we made these role transitions easier. In reality the forces influencing these role transitions are decidedly mixed with considerable government pressure making them harder. We have, just to take one example, qualified investor rules limiting certain investment opportunities only to the well off that are completely out of place in a world that has undergone an information revolution.

There's a four page run where Piketty is acknowledging his colleagues and making a few technical points. Nothing to complain about there, and thank goodness for pacing issues in this analysis.

But page 20 has a bit of interesting caution to not accept any economic determinism, walking back Piketty's page 15 straight line analysis about who will own the world in 2050 or 2100. Piketty anticipates critics and refutes himself.

Piketty asserts that "there is no natural, spontaneous process to prevent destabilizing, inegalitarian forces from prevailing permanently." This is wrong as there is a powerful one, human nature. Those who are rich tend towards complacency and those who are poor tend towards activity. You have to work hard to beat the poor down into giving up, especially in a world of cheap information and huge gaping holes of unfulfilled goods and services. As this is a major result of the study that the book is based on, Piketty is in trouble long before he pulls out his first spreadsheet because, like Marx, he doesn't get people right. Let us hope it is with less momentous consequences.

It is really breathtaking, Piketty's idea that the market has little to do with the catch up in economies that are happening in a number of formerly poor economies. A key portion of the "process of the diffusion and sharing of knowledge" that is driving that catch up is that markets work and it is wise to dismantle the legal structures that prohibited or restricted markets in these countries. But for Piketty, that sort of knowledge diffusion is a priori not important.

In the forces of convergence section, there is a great elephant of a void, one that is quite noticeable if you don't have Piketty's sort of ideological blinders on. Over time, if you are prudent, you can move from being a laborer to a capitalist, and it would be normal that there are a large number of people who gain income from doing both and shifting emphasis from one to another as a counterbalancing force, chasing the better deal.

If capitalist activities are where the money is, there would be a natural tendency to increase effort in those areas and to divert income to investments, bidding up the prices and thus reducing the returns on capital. The sort of world where there's a tiny class of investors and everybody else gets all their income from labor is simply not today's world. This is exactly the sort of evolution that supports the Kuznets curve. That we're presently sabotaging this evolution via a huge creation of moral hazard by central banks and other policy stupidities does not change the underlying reality that humans tend to follow the money when it comes to earning their daily bread and Piketty's book is largely devoted to the proposition that they do not.

If you give short shrift to and do not accurately list the forces for convergence, of course they will look weak and easily overcome by forces for divergence. Again, this is an argument that does not depend on Piketty's statistics being in error, though the argument would be consistent with the errors that the FT found in its analysis.

Once again, I have reached the point where it is too long to go much further on a blog post and will try to pick things up again later.

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 15 on the introduction.

On page 15 there's an interesting concept introduced of "inequalities at the global level" that leaves me scratching my head. China "may well prove to be a potent force for reducing inequalities on the global level" but isn't China's turning towards capitalism mean that its headed towards more inequality? What is different (superior?) about the Chinese road towards the market? Before Deng, what was China's role regarding inequality on a global level? I would hope that Piketty explores this more fully later. We'll see.

The idea that you can make any sort of straight line trends in global economics last 35 years, much less 85 years with a straight face is in my mind, well, naive at best. But Piketty goes for it even as he makes sure to inject enough uncertainty in his projections to make this statement meaningful. In other words, he's dog whistling about the world ending up being owned due to the straight line projection across several decades. If anybody of influence were to call him on this, no doubt he would retreat, and quickly. From the media appearances I've observed, he's obviously not enough of an idiot to defend such a declaration, though he is enough of one to have made it in the first place.

An interesting assumption embedded in Piketty's snark about Solow and Kuznets "balanced growth path" is that the rich world is advanced in the sense that Solow and Kuznets meant. That's not actually proven. For instance in the 1970s, the US made a retrograde move that established an oligarchy in bond rating agencies, one that continues to this day. How many other retrograde moves have been made and what does that mean in the sense of the Kuznets curve? There's plenty of pages to go and perhaps Piketty addresses this later but it is as absurd to assume that capitalism is a one way road. As Newsweek famously observed in 2009 "we are all socialists now." Has this socialism turned back the clock on the Kuznets curve? Is that even on Piketty's radar?

The 19th century economists, especially Marx, underestimated the mobility of people to change roles when the legal system permits them to and the economic system incentivises them to. Our economy would be more balanced if we made these role transitions easier. In reality the forces influencing these role transitions are decidedly mixed with considerable government pressure making them harder. We have, just to take one example, qualified investor rules limiting certain investment opportunities only to the well off that are completely out of place in a world that has undergone an information revolution.

There's a four page run where Piketty is acknowledging his colleagues and making a few technical points. Nothing to complain about there, and thank goodness for pacing issues in this analysis.

But page 20 has a bit of interesting caution to not accept any economic determinism, walking back Piketty's page 15 straight line analysis about who will own the world in 2050 or 2100. Piketty anticipates critics and refutes himself.

Piketty asserts that "there is no natural, spontaneous process to prevent destabilizing, inegalitarian forces from prevailing permanently." This is wrong as there is a powerful one, human nature. Those who are rich tend towards complacency and those who are poor tend towards activity. You have to work hard to beat the poor down into giving up, especially in a world of cheap information and huge gaping holes of unfulfilled goods and services. As this is a major result of the study that the book is based on, Piketty is in trouble long before he pulls out his first spreadsheet because, like Marx, he doesn't get people right. Let us hope it is with less momentous consequences.

It is really breathtaking, Piketty's idea that the market has little to do with the catch up in economies that are happening in a number of formerly poor economies. A key portion of the "process of the diffusion and sharing of knowledge" that is driving that catch up is that markets work and it is wise to dismantle the legal structures that prohibited or restricted markets in these countries. But for Piketty, that sort of knowledge diffusion is a priori not important.

In the forces of convergence section, there is a great elephant of a void, one that is quite noticeable if you don't have Piketty's sort of ideological blinders on. Over time, if you are prudent, you can move from being a laborer to a capitalist, and it would be normal that there are a large number of people who gain income from doing both and shifting emphasis from one to another as a counterbalancing force, chasing the better deal.

If capitalist activities are where the money is, there would be a natural tendency to increase effort in those areas and to divert income to investments, bidding up the prices and thus reducing the returns on capital. The sort of world where there's a tiny class of investors and everybody else gets all their income from labor is simply not today's world. This is exactly the sort of evolution that supports the Kuznets curve. That we're presently sabotaging this evolution via a huge creation of moral hazard by central banks and other policy stupidities does not change the underlying reality that humans tend to follow the money when it comes to earning their daily bread and Piketty's book is largely devoted to the proposition that they do not.

If you give short shrift to and do not accurately list the forces for convergence, of course they will look weak and easily overcome by forces for divergence. Again, this is an argument that does not depend on Piketty's statistics being in error, though the argument would be consistent with the errors that the FT found in its analysis.

Once again, I have reached the point where it is too long to go much further on a blog post and will try to pick things up again later.

Saturday, June 7, 2014

Piketty's Introduction - Part II

This is a four part series going through Thomas Piketty's Capital in the 21st Century the parts can be found here:

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 7 on the introduction.

Wages are not hard linked to economic growth in capitalism. Wages are an epiphenomenon of the supply and demand of labor. With the countryside emptying out in a rush during the early industrial revolution, capital and labor became strongly unbalanced. The reasons for this were good. Increased yields from new technology led to less starvation and less need for farm labor. Unsurprisingly this led to low and stagnant wages at the urban receiving end until this huge wave of labor was absorbed and capital pools grew to a level that led to the bidding up of wages as capitalists had to start to compete for workers in a more serious way. Nobody who has gotten past undergraduate economics should be surprised, yet Professor Piketty seems surprised writing about the period "[t]his long period of wage stagnation, which we observe in Britain as well as France, stands out all the more because economic growth was accelerating in this period." This seems to be coming from a milieu of social justice and not economics. That would be fine if this were not an economics book. Or is it?

On page 9, Piketty passes over one of the greatest failures of Marx, the pretense that his vision of communism was scientific. A scientific communism is a communism that runs an experiment and when the experiment fails, it stops. Marxism never stops. It just gets new excuses.

It's only page 10 and Piketty seems to be undermining one of his previous statements that inequality inevitably leads to violence with the observation that inequality still was increasing in WW I but since wages were catching up, the spectre of proletarian revolution was receding in the advanced industrialized world. Is this what he means by "modern" economic growth? There's nothing particularly modern about absorbing and correcting a surplus of labor with the creation of new enterprises to occupy them.

Piketty is once again unduly kind to Marx by excusing his failure on a lack of statistical information. "If only the [great man] had known" is the cry of suckers who believe in failed systems and Piketty is engaging in that a bit here. It is particularly relevant to note that Marx's labor theory of value does not work. Marx raised important questions. So can a five year old. Such an act, unaccompanied by correct answers is not the stuff of greatness. Here Marx, have a cookie for asking an interesting question. Now go stand in the corner of historical villainy for making the gulag possible. Piketty has lousy taste.

Accumulated wealth is ultimately of two sources, gathered and/or maintained by violence or gathered/maintained by skill. The former is to be condemned and fought against. The latter is intergenerationally unreliable (ie over the scale of time that generates social instability). Societal measures should target only the first. Piketty's preferred solution to the problem targets both. People do not go out into the streets to fight against Bill Gates riches in relevant numbers because manifestly he is doing a world of good, as do many of his peers. The Democrat party's obsession with the Koch brothers is relevant here. Explaining both why the Democrats have made them their great white whale and why ultimately it's not giving them the political traction they hoped.

Piketty is in love with statistics and so I see why he might think that income tax is "useful for establishing classifications and promoting knowledge as well as democratic transparency" in his discussion on Kuznets. The usefulness of this information is a bit counterbalanced by the enabling effect on envy and the almost inevitable reduction of societal solidarity. Pity he doesn't mention those effects. They must not fit his narrative. In a book devoted to the ill effects of inequality, it's a little surprising that he's overlooking this contribution to those ill effects.

Kuznets, with his eponymous curve, seems to be the big elephant that Piketty is aiming at. He calls it "magical", a term not usually professionally complimentary. Kuznets must be discredited for Piketty's thesis of dangerously growing inequality to have a chance. The Kuznets curve was "a product of the Cold War" which implies but does not say that it is wrong. The moon landing was a product of the Cold War. Does Piketty cast doubt on that because of its provenance too? Let's try it on for size, the "magical Kuznets curve" matched by the magical moon landing? I think not.

The Kuznets curve will stand or fall as we end up in a sufficiently long period without huge exogenous shocks that mask the effect if it's present. Piketty's snark doesn't move the conversation along.

Once again this is getting too long for a blog post. If I keep up this pace of analysis, I will be posting another 81 posts on this book. I may have to take lessons from Stephen Green towards the end. I don't think I'm going to make it in six more days. As annoying as finding these problems in Piketty's work, the thing is intellectually stimulating, probably in ways that Piketty didn't intend. For instance, it seems like under Piketty's analysis of global inequality, communism was anti-egalitarian. Now that would be an interesting interview question for Piketty but unlikely one that he would face.

Part I, Part II, Part III, Part IV

After only suspecting it from press accounts, picking up Piketty's Capital in the Twenty-First Century has convinced me by the second paragraph of its introduction that it desperately needs a thorough fisking. I'm picking up here from page 7 on the introduction.

Wages are not hard linked to economic growth in capitalism. Wages are an epiphenomenon of the supply and demand of labor. With the countryside emptying out in a rush during the early industrial revolution, capital and labor became strongly unbalanced. The reasons for this were good. Increased yields from new technology led to less starvation and less need for farm labor. Unsurprisingly this led to low and stagnant wages at the urban receiving end until this huge wave of labor was absorbed and capital pools grew to a level that led to the bidding up of wages as capitalists had to start to compete for workers in a more serious way. Nobody who has gotten past undergraduate economics should be surprised, yet Professor Piketty seems surprised writing about the period "[t]his long period of wage stagnation, which we observe in Britain as well as France, stands out all the more because economic growth was accelerating in this period." This seems to be coming from a milieu of social justice and not economics. That would be fine if this were not an economics book. Or is it?

On page 9, Piketty passes over one of the greatest failures of Marx, the pretense that his vision of communism was scientific. A scientific communism is a communism that runs an experiment and when the experiment fails, it stops. Marxism never stops. It just gets new excuses.

It's only page 10 and Piketty seems to be undermining one of his previous statements that inequality inevitably leads to violence with the observation that inequality still was increasing in WW I but since wages were catching up, the spectre of proletarian revolution was receding in the advanced industrialized world. Is this what he means by "modern" economic growth? There's nothing particularly modern about absorbing and correcting a surplus of labor with the creation of new enterprises to occupy them.

Piketty is once again unduly kind to Marx by excusing his failure on a lack of statistical information. "If only the [great man] had known" is the cry of suckers who believe in failed systems and Piketty is engaging in that a bit here. It is particularly relevant to note that Marx's labor theory of value does not work. Marx raised important questions. So can a five year old. Such an act, unaccompanied by correct answers is not the stuff of greatness. Here Marx, have a cookie for asking an interesting question. Now go stand in the corner of historical villainy for making the gulag possible. Piketty has lousy taste.

Accumulated wealth is ultimately of two sources, gathered and/or maintained by violence or gathered/maintained by skill. The former is to be condemned and fought against. The latter is intergenerationally unreliable (ie over the scale of time that generates social instability). Societal measures should target only the first. Piketty's preferred solution to the problem targets both. People do not go out into the streets to fight against Bill Gates riches in relevant numbers because manifestly he is doing a world of good, as do many of his peers. The Democrat party's obsession with the Koch brothers is relevant here. Explaining both why the Democrats have made them their great white whale and why ultimately it's not giving them the political traction they hoped.

Piketty is in love with statistics and so I see why he might think that income tax is "useful for establishing classifications and promoting knowledge as well as democratic transparency" in his discussion on Kuznets. The usefulness of this information is a bit counterbalanced by the enabling effect on envy and the almost inevitable reduction of societal solidarity. Pity he doesn't mention those effects. They must not fit his narrative. In a book devoted to the ill effects of inequality, it's a little surprising that he's overlooking this contribution to those ill effects.

Kuznets, with his eponymous curve, seems to be the big elephant that Piketty is aiming at. He calls it "magical", a term not usually professionally complimentary. Kuznets must be discredited for Piketty's thesis of dangerously growing inequality to have a chance. The Kuznets curve was "a product of the Cold War" which implies but does not say that it is wrong. The moon landing was a product of the Cold War. Does Piketty cast doubt on that because of its provenance too? Let's try it on for size, the "magical Kuznets curve" matched by the magical moon landing? I think not.

The Kuznets curve will stand or fall as we end up in a sufficiently long period without huge exogenous shocks that mask the effect if it's present. Piketty's snark doesn't move the conversation along.

Once again this is getting too long for a blog post. If I keep up this pace of analysis, I will be posting another 81 posts on this book. I may have to take lessons from Stephen Green towards the end. I don't think I'm going to make it in six more days. As annoying as finding these problems in Piketty's work, the thing is intellectually stimulating, probably in ways that Piketty didn't intend. For instance, it seems like under Piketty's analysis of global inequality, communism was anti-egalitarian. Now that would be an interesting interview question for Piketty but unlikely one that he would face.

Friday, June 6, 2014

Piketty's Introduction - Part I

This is a four part series going through Thomas Piketty's Capital in the 21st Century the parts can be found here:

Part I, Part II, Part III, Part IV

Piketty's introduction is the first problem with the book. He manages to get through paragraph one without serious problems but can't manage to extend that record to paragraph two.

Piketty claims

It's only the introduction but it's not looking good so far. Piketty has already revealed that he is assuming his conclusions.

It gets worse

An illustration should suffice. Take a room full of poor entrepreneurs. Add exactly one money bags investor. The economy will rely on the investor to supply virtually all the capital. Assume that out of 100 business proposals he funds 10 and being the only game in town he does so at quite advantageous terms to himself. 1 is a 100x investment success, 6 are variously successful averaging 4x return, and 3 go bust. The return to capital is clearly going to be greater than economic growth in this situation. But the 100x successful business yields enough money in the heretofore poor entrepreneurs hands that he can fund a venture all by himself and the 6 entrepreneurs can fund another 2 if they act together. The next funding round sees essentially 4 money bags and more businesses being funded. Each subsequent round will see less and less lopsided terms being granted the entrepreneurs. After all, they can play one investor off against another. More and more of the poor entrepreneurs will either propose or be part of a successful team. More and more deals will be self-financed. Eventually you get to a balance. This is the deep structure of capitalism and it is very different from what Piketty is assuming.

Now add Piketty's famous wealth tax and what happens. The money bags won't be investing in 10 businesses, but 7, the balance of his funds being absorbed by tax shelters and lobbying for loopholes in the wealth tax (which empirical observation leads us to guess that he will get but that it absorbs a large amount of time, effort, and money). The 100x entrepreneur winner in the first round might still be comfortable but likely not enough to fund the same sort of venture as before and the medium sized winners are fewer and even less capable of enlarging the pool of investors and increasing the fairness of terms in the next round of investment in business.

Piketty is trying to claim a moral high ground as early as page 1 but unfortunately for him, he is a policy villain. He seems to ignore that R > G is a price signal. This price signal is an encouragement to enter the field of capitalist and invest. Taxing the wealthy is a strong signal not to invest too much, diverting resources.

Piketty claims that "violent political conflict" is something that "inequality inevitably instigates". I look forward to seeing the data that proves this claim because I do not believe it to be true. Comfortable members of the middle class are not going to be going out into the streets because the rich are getting more comfortable faster. They are especially not going to be doing it when the path to their own riches clearly remains open if they wish to exert themselves. Inequality, per se, does not lead to violence. Additional factors have to be present.

I'll leave a placeholder here regarding Piketty's discussion on oil prices and urban land as he explicitly says that he'll provide a nuanced discussion later. Suffice to say his introductory remarks do not instill confidence. That the Chinese have (wisely or foolishly) built many empty cities demonstrates that increasing the supply of urban land is not that difficult. As for oil, there is a ceiling price to oil, and it's dropping. Fischer Tropsch plants can convert other hydrocarbons to liquid fuels. So long as the extensive investment costs can be recovered, a persistent level of high oil prices is simply not going to happen and that is putting aside the more exotic substitute goods of electric and fuel cell powered vehicles.

We are barely into page 7 of a 35 page introduction and this is already getting long for a blog post so I will stop here and add a 'part I' to my title.

Update: Piketty partially addresses the issue of substitute goods in footnote 3. I say partially because he claims that finding these substitute goods "can take decades to accomplish" which is weasel wording at best. Modern economies research pieces of substitute goods, often decades before they are generally needed and leave the results in patent offices and scientific journal, dormant until we approach the conditions where they become practical whereupon the vision of riches leads to their resurrection more often than not. Large price swings actually create a positive influence in this process as can be seen in the fits and starts refinement process that has made Fischer Tropsch a practical substitute good for drilling oil. At this point, it is only the long lead times for recouping investment and the uncertainty of how quickly other substitute goods for transportation fuel will emerge that are holding back this technology.

it's become clear to me that footnotes are where Piketty is going to be burying the inconvenient facts he must cover to save his reputation while minimizing the number of people who actually walk away with an appreciation of those facts. This is not quite an approach that is devoted to the honest search for truth.

Part I, Part II, Part III, Part IV

Piketty's introduction is the first problem with the book. He manages to get through paragraph one without serious problems but can't manage to extend that record to paragraph two.

Piketty claims

Modern economic growth and the diffusion of knowledge have made it possible to avoid the Marxist apocalypse but have not modified the deep structures of capital and inequality.But that's just not right. What is it about modern economic growth that makes it Marx bane as opposed to pre-modern economic growth? Piketty doesn't say up front. Perhaps later, but there doesn't seem to be much discussion of it uncovered by a Google search. The concept of a magical 'modern' economic growth doesn't make much sense. The diffusion of knowledge makes a very vague reference to the real issue of R > G but not in a particularly helpful way. Isn't the very existence of deep structures of capital and inequality the question that Piketty is putatively seeking to answer, ie whether Marx was right all along?

It's only the introduction but it's not looking good so far. Piketty has already revealed that he is assuming his conclusions.

It gets worse

When the rate of return on capital exceeds the rate of growth of output and income... capitalism automatically generates arbitrary and unsustainable inequalities that radically undermine the meritocratic values on which democratic societies are based.This is simply not true. You have to have an additional factor for an undermining effect to take place. You have to limit the conversion of individuals who live via labor to individuals who earn a living via capital. There are plenty of people who work to pull up the ladder that enables this conversion but they do not generally reside among the advocates of laissez faire. Piketty's advertised solution, a heavy wealth tax, pulls up the ladder quite effectively. This makes Piketty a decided villain by his own R > G standards.

An illustration should suffice. Take a room full of poor entrepreneurs. Add exactly one money bags investor. The economy will rely on the investor to supply virtually all the capital. Assume that out of 100 business proposals he funds 10 and being the only game in town he does so at quite advantageous terms to himself. 1 is a 100x investment success, 6 are variously successful averaging 4x return, and 3 go bust. The return to capital is clearly going to be greater than economic growth in this situation. But the 100x successful business yields enough money in the heretofore poor entrepreneurs hands that he can fund a venture all by himself and the 6 entrepreneurs can fund another 2 if they act together. The next funding round sees essentially 4 money bags and more businesses being funded. Each subsequent round will see less and less lopsided terms being granted the entrepreneurs. After all, they can play one investor off against another. More and more of the poor entrepreneurs will either propose or be part of a successful team. More and more deals will be self-financed. Eventually you get to a balance. This is the deep structure of capitalism and it is very different from what Piketty is assuming.

Now add Piketty's famous wealth tax and what happens. The money bags won't be investing in 10 businesses, but 7, the balance of his funds being absorbed by tax shelters and lobbying for loopholes in the wealth tax (which empirical observation leads us to guess that he will get but that it absorbs a large amount of time, effort, and money). The 100x entrepreneur winner in the first round might still be comfortable but likely not enough to fund the same sort of venture as before and the medium sized winners are fewer and even less capable of enlarging the pool of investors and increasing the fairness of terms in the next round of investment in business.

Piketty is trying to claim a moral high ground as early as page 1 but unfortunately for him, he is a policy villain. He seems to ignore that R > G is a price signal. This price signal is an encouragement to enter the field of capitalist and invest. Taxing the wealthy is a strong signal not to invest too much, diverting resources.

Piketty claims that "violent political conflict" is something that "inequality inevitably instigates". I look forward to seeing the data that proves this claim because I do not believe it to be true. Comfortable members of the middle class are not going to be going out into the streets because the rich are getting more comfortable faster. They are especially not going to be doing it when the path to their own riches clearly remains open if they wish to exert themselves. Inequality, per se, does not lead to violence. Additional factors have to be present.

I'll leave a placeholder here regarding Piketty's discussion on oil prices and urban land as he explicitly says that he'll provide a nuanced discussion later. Suffice to say his introductory remarks do not instill confidence. That the Chinese have (wisely or foolishly) built many empty cities demonstrates that increasing the supply of urban land is not that difficult. As for oil, there is a ceiling price to oil, and it's dropping. Fischer Tropsch plants can convert other hydrocarbons to liquid fuels. So long as the extensive investment costs can be recovered, a persistent level of high oil prices is simply not going to happen and that is putting aside the more exotic substitute goods of electric and fuel cell powered vehicles.

We are barely into page 7 of a 35 page introduction and this is already getting long for a blog post so I will stop here and add a 'part I' to my title.

Update: Piketty partially addresses the issue of substitute goods in footnote 3. I say partially because he claims that finding these substitute goods "can take decades to accomplish" which is weasel wording at best. Modern economies research pieces of substitute goods, often decades before they are generally needed and leave the results in patent offices and scientific journal, dormant until we approach the conditions where they become practical whereupon the vision of riches leads to their resurrection more often than not. Large price swings actually create a positive influence in this process as can be seen in the fits and starts refinement process that has made Fischer Tropsch a practical substitute good for drilling oil. At this point, it is only the long lead times for recouping investment and the uncertainty of how quickly other substitute goods for transportation fuel will emerge that are holding back this technology.

it's become clear to me that footnotes are where Piketty is going to be burying the inconvenient facts he must cover to save his reputation while minimizing the number of people who actually walk away with an appreciation of those facts. This is not quite an approach that is devoted to the honest search for truth.

The weakness of Piketty's critics

I have not had the opportunity to read all of Piketty's critics so it is quite possible that I am unjust but the ones that have gotten the most play are weak critiques to my view and are doomed to failure because they grant Piketty too much credit. The FT critique, which I find interesting, is useless without challenging Piketty much earlier in the book, which they fail to do. The numbers work is great, as is to some extent Piketty's. The fatal problem with Piketty was alway going to be elsewhere.

I'm going to be doing a bit of fisking on Piketty's book. I think I can manage it if I write while I read. Absent that, somebody would have to pay me for the necessary time and then I would put out a much better product. Since the likelihood of manna from heaven is slight, I'm just going to have to risk critiquing as I go along and retracting/correcting if later chapters fill the gaps and errors I spot.

I'm going to be doing a bit of fisking on Piketty's book. I think I can manage it if I write while I read. Absent that, somebody would have to pay me for the necessary time and then I would put out a much better product. Since the likelihood of manna from heaven is slight, I'm just going to have to risk critiquing as I go along and retracting/correcting if later chapters fill the gaps and errors I spot.

Library Follies

My local library highly estimates the reading ability of Lake County, IN library patrons. They made Thomas Piketty's Capital in the Twenty First Century a seven day loan book. Not counting footnotes, it's a 577 page book.

I'll give it a shot.

I'll give it a shot.

Subscribe to:

Posts (Atom)